Robots, pandemics and inequality; Interest rates, house prices, and financial crises; Emergency money; Digital Euro

Your dose of nonsense - Monday, 2021-04-26

If you liked this, consider liking, subscribing and forwarding. You know, for the algos. If you didn’t like it, consider forwarding it to someone you don’t like.

Robots, pandemics and inequality

I think that we collectively have a love-hate relationship with automation.

We love it when it takes care of all the dull, boring chores away from us. Like, say, a washing machine. Okay, I don’t love my washing machine, but I love it that I don’t have to go out to find a river while carrying a large wash basin and a washing board to do my laundry.

But while we may nearly all universally agree today that doing our laundry manually is a dull, boring and tedious chore that we wish would just “go away”, if we bring this up one level, thanks to the diversity of humankind, the line between “dull and boring” and “interesting” is less clear. While some of you may consider baking a chore (and hence, you buy your baked goods from some bakery, or you fall into the fad of buying a breadmaker, use it for a month, then shove it somewhere and go back to buying baked goods), others might really enjoy the manual process of baking.

Then at the next level, we have activities that we depend on to make a living. Like manufacturing, for example. While many of us see it as a chore to make something ourselves, there are probably equally as many who depend on it to put food on the table and a roof over their heads.

But you see, for many people who run and own the factories, it’s exactly the “food” and “roof” bits that they think are not really efficient. Humans workers need time off to eat, sleep, and do other recreational activities. Robots don’t. If you want to ethically run a factory 24-hours a day, you would probably need to hire at the very least 3 sets of staff, one set for an 8-hour shift. On the other hand, you only need one set of robots. Hence, there’s always the incentive to automate using robots.

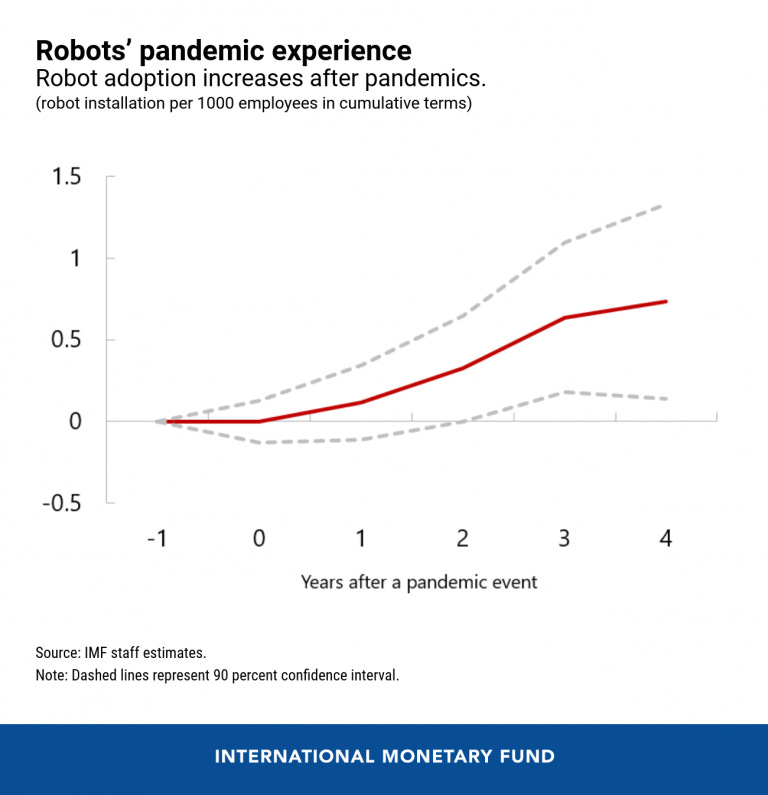

But what if one day, you, the plant owner, find that you aren’t able to get any of your shifts of workers in? Say, because of a pandemic? Now, you have one more incentive to automate as much as you can. And according to the International Monetary Fund, that’s what we have done over the past few pandemics.

Using SARS in 2003, H1N1 in 2009, MERS in 2012, and Ebola in 2014 outbreak data, they have reported in this blog post that robot adoption has historically increased after a pandemic, as shown in the graph below:

Source: IMF

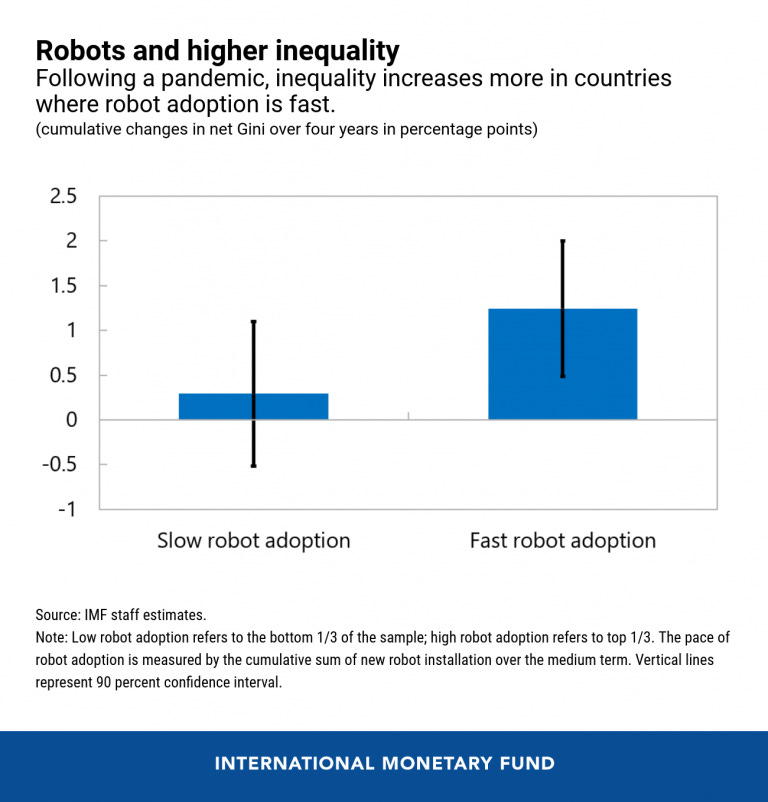

And in the same blog post, they have also reported that inequality (as measured by the change in the Gini coefficient) increases with increased use of robots:

Source: IMF

So what’s next for us humans? Is it time for us to upload our consciousness onto “the cloud” where we are immune to biological pathogens and can work 24/7/365 (if you are willing to only work your entire life, that is)?

(Probably not. I mean, robots do get infected by viruses too, just not biological ones.)

Interest rates, house prices, and financial crises

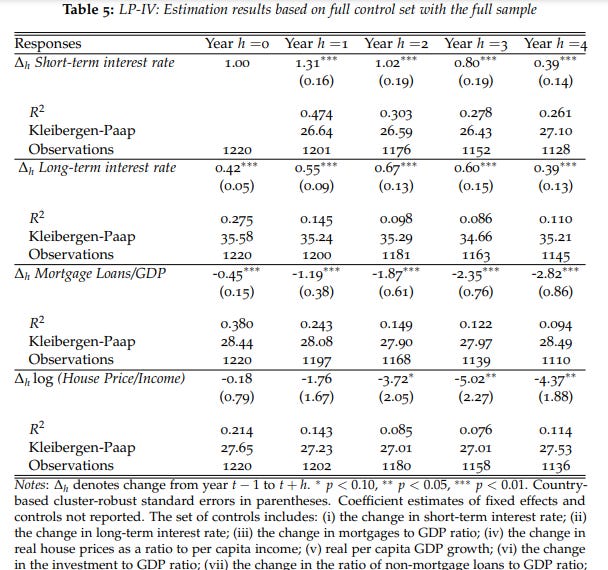

I don’t know about you, but I take it for granted that when interest rates are low, house prices would go up. I mean, if you were able to borrow cheaply, wouldn’t you like to do so?

But some people, and rightly so, refuse to simply take that relationship as self evident, and look at the data themselves. This 2014 National Bureau Of Economic Research paper looks at 140 years worth of data to establish if looser monetary conditions does indeed raise house prices. Their conclusion was it does*. The table below shows that whatever historical factors that make interest rates go up (first two rows, note the positive numbers), would make house prices go down (last row, note the negative numbers):

Source: National Bureau Of Economic Research

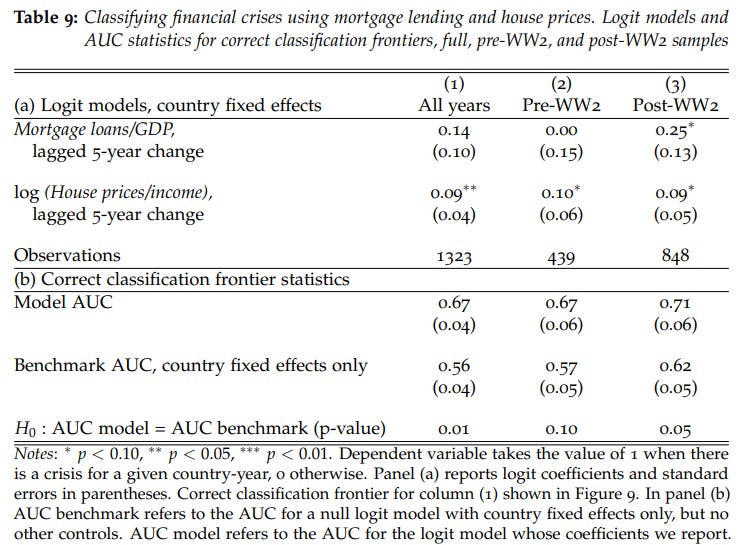

They also go one step further by making the assertion that housing bubbles increase the risk of financial crises. The table below shows that the two metrics,

Mortgage loans as a proportion of Gross Domestic Product; and

House prices as a multiple of income

have some relationship with financial crises:

Source: National Bureau Of Economic Research

So here’s a conundrum that central bankers face today. With low interest rates and high property prices in the UK, for example, if the Bank of England were to raise interest rates for whatever reason (e.g. inflation), house prices might go down. But people are more likely to spend money when they feel rich, and less likely to when they feel poor. (Some people call this phenomenon the “wealth effect”, and here’s the Bank of England explaining it). But if they raise rates too quickly, this may cause house prices to fall, thus discouraging people to spend their money, which in turn would likely affect the recovery of the economy.

I guess it’s a tough job being a central banker.

* Footnote: except Germany. Despite having low interest rates, as a whole, Germans didn’t quite like (and maybe still don’t like?) housing loans as much as other countries. Which is probably why the German banks had to seek their fortunes elsewhere, such as this Las Vegas casino that Deutsche used to own and “spared no expense” on the decor. Also regional banks BayernLB, WestLB, LBBW and HSH Nordbank had around €80 billion worth of exposure to US subprime mortgages. For context, Deutsche Bank’s current value (of its shares) is roughly €25 billion.

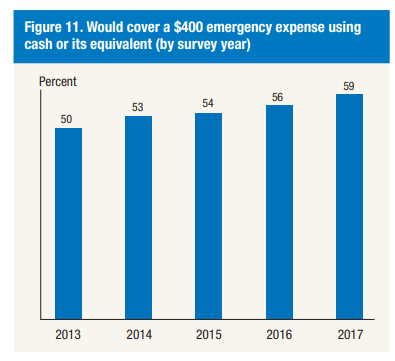

Emergency money

If you were suddenly hit by an unexpected £400 / $400 bill, would you be able to find enough money to pay it off today?

The US Federal Reserve found in a 2018 survey that 40% of Americans couldn’t.

Source: US Federal Reserve

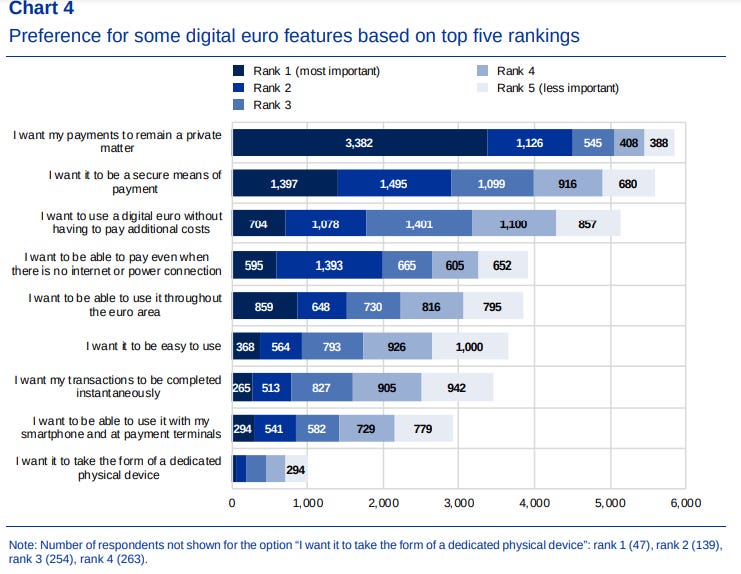

Digital Euro Survey

The European Central Bank carried out a public consultation on a digital Euro. You know, everyone is talking about Bitcoin, Dogecoin and China’s digital yuan. Digital currencies are all the rage now. The EU certainly doesn’t want to feel left out.

Even the UK is considering one:

Source: Twitter

So what do Europeans want from their digital currency? Well, I guess with little surprise, they favour privacy the most:

Source: ECB

PS: None of my content is sponsored content. All opinions are my own. Nothing in this newsletter is investment, legal, business, medical, or life advice (my subtitle is “Your daily dose of nonsense”). Don’t be believing everything a random guy on the internet says.